Why VW and Bosch backed the wrong AV brain architecture

Volkswagen is reportedly winding down its Automated Driving Alliance with Bosch. Launched in 2022 with $1.71 billion committed, the partnership set out to build a competitive software stack for advanced driver assistance and automated driving — targeting Level 2++, Level 3 autonomous driving, and beyond.

Four years later, the internal conclusion at VW is blunt: the technology is not competitive. This stings not because Bosch lacks excellence or VW lacked effort. Bosch is world-class. VW poured resources into fixing its software organisation. Autonomous driving remains one of the hardest problems in engineering. The real pain is that this outcome was visible in 2022 — if you were tracking the right signal.

The market will frame this as another chapter in VW's software struggles: CARIAD complexity, execution delays, internal politics, supplier dependencies. Those factors played a role. But the deeper mistake was architectural — and it was measurable through patent analytics long before it became a public reset.

The data called it the year they signed

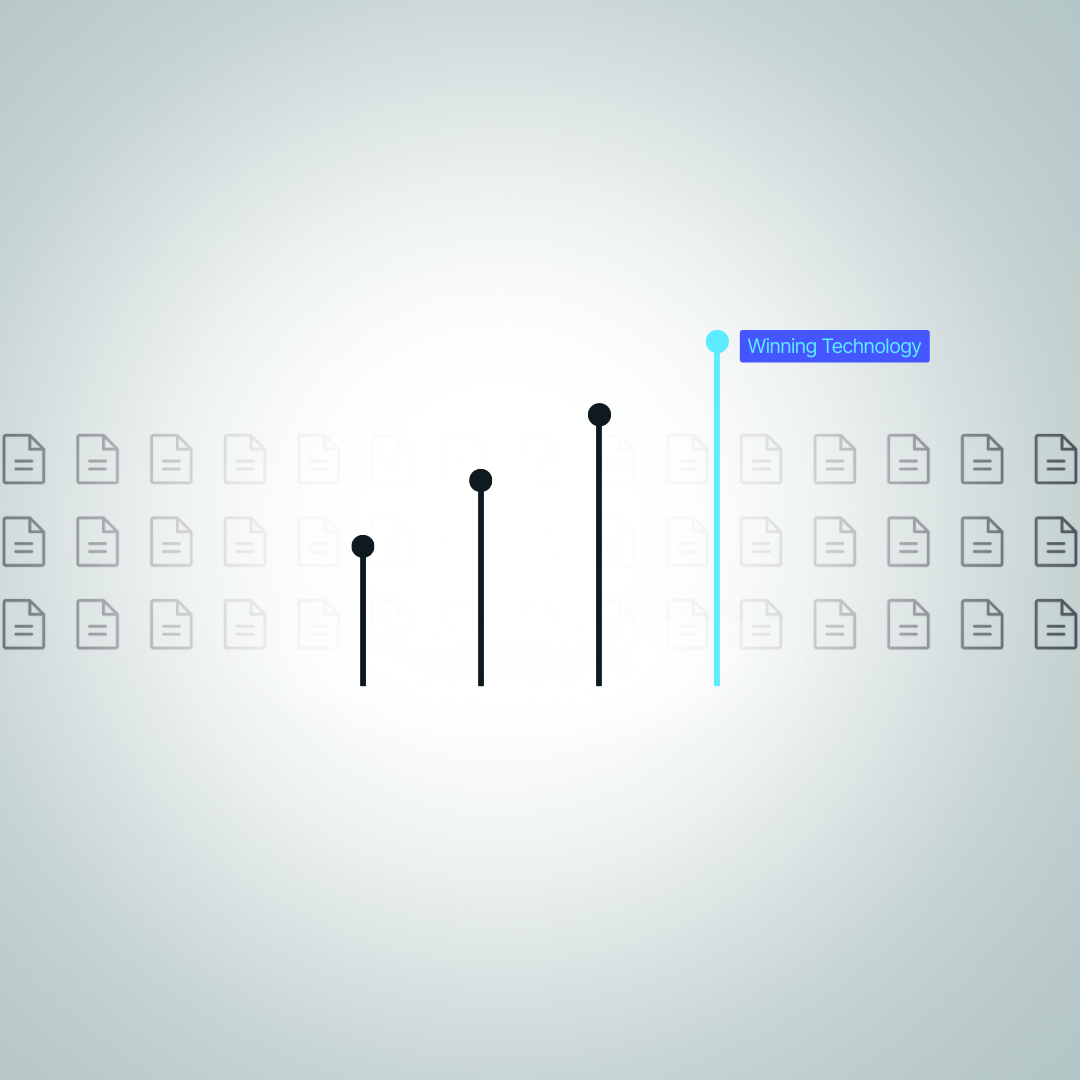

Could Volkswagen and Bosch have known, in 2022, that they were committing to the wrong AV brain architecture? Yes. The year they committed ~$1.71B to a classical modular pipeline, GetFocus improvement-rate data already showed a different architecture — modular end-to-end — pulling decisively ahead of every alternative. At signing it was improving 2.6× faster; by 2023 the lead was 3.5×, and the route they chose had started to decline.

This is what technology scouting with GetFocus does: we quantify improvement rates across technology domains using patent citation dynamics, recency and impact. Improvement Rate is not a lagging indicator of activity — it is a leading signal of which architectures are compounding fastest and pulling away from the pack.

See exactly how we calculate it in the GetFocus Technology Improvement Rate methodology explainer.

They backed the architecture the signal was leaving behind

Bosch and VW's CARIAD built what they called a "modular, scalable AI stack" — separate perception, intent, planning and execution modules, each validated independently. It is a defensible engineering position, and Bosch is world-class. But it is structurally classical modular — not the unified, interpretable-by-design architecture the improvement-rate signal had already moved to.

Each classical module optimises for its local objective and compresses the world before handing it off. Uncertainty gets lost. Errors compound. Iteration is slow, because a change in one module ripples across the whole system. Modular end-to-end changes the game: it preserves useful structure while letting gradients and learning flow across larger portions of the stack, so the system learns representations optimised for the final driving outcome rather than for intermediate hand-offs. That enables faster compounding: more data → better model → better driving → more deployment → more data.

Improvement rate is the only forward-looking signal

Tesla accelerated its shift toward end-to-end neural driving (visible in FSD v12 and beyond, with v14 shifting further the same way in late 2025), pushing more of the stack into learned behaviour trained on a massive real-world fleet. Chinese players — Momenta, Horizon Robotics, XPeng, BYD and others — moved aggressively into large-model, data-driven systems. They are not waiting for perfect modular validation; they are iterating through the data loop at speed. Classical modular stacks still improve — but they do not compound at the same rate, and eventually the architecture itself becomes the bottleneck.

We have seen this exact pattern before. In batteries, LFP's improvement rate was ahead of NMC years before the 2020–21 commercial inflection — the signal led consensus by about six years. In the AV brain race the same mechanism is playing out, only faster: a 3–4 year lag from signal to public correction.

Source : Sodium-Ion vs LFP: Predicting the Next Battery Disruption with Patent Data

Everything else in the standard toolkit — filing volumes, top assignees, headlines, launches, demo reels — is a rear-view mirror. Improvement rate is the rate at which each architecture is advancing on the cost/performance frontier. It moves before the market does.

Where each architecture lands, and what to do

The VW–Bosch story is not primarily about one failed partnership. It is a textbook example of how large organisations lose technology races: they make reasonable decisions based on outdated signals — supplier reputation, current capability, internal comfort, perceived controllability — while ignoring the rate at which competing architectures are improving. This is the core of modern R&D strategy and technology forecasting: patent data, read for genuine momentum and acceleration, reveals which technologies are pulling away long before market outcomes make it obvious.

Ready to see it in action?

Discover how GetFocus can transform your strategic decision-making process today.